Article Summary –

The Inflation Reduction Act of 2022 (IRA) introduces significant changes to Medicare Part D, including eliminating the coverage gap, capping out-of-pocket costs at $2,000, and altering cost-sharing responsibilities among beneficiaries, plan sponsors, drug manufacturers, and the government starting from January 1, 2025. These changes are expected to relieve many beneficiaries by reducing their costs and out-of-pocket expenses, but they could also result in increased premiums and more restrictive formularies from PDPs, who will bear more financial risk. Manufacturers might experience varied impacts, with brand drug manufacturers potentially benefiting from reduced discount obligations but facing shifts in formulary placements and rebate dynamics.

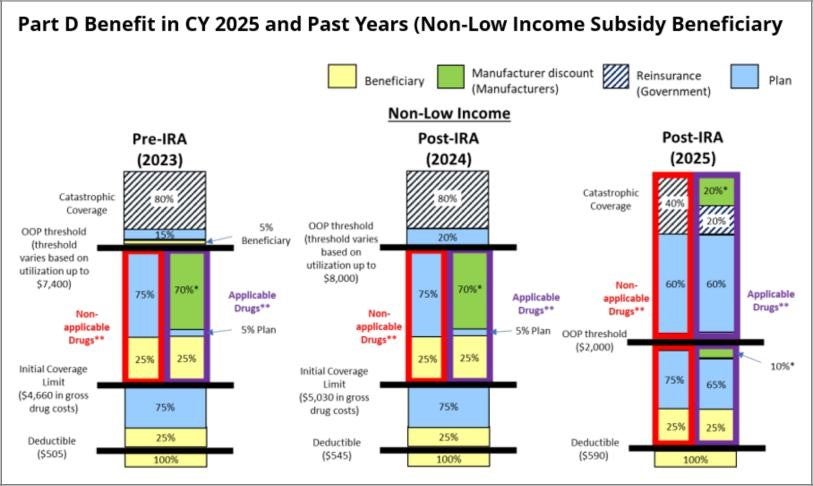

The Inflation Reduction Act of 2022 (IRA) marked a significant milestone in Congress’s efforts to address escalating health care costs. It aims to reduce government spending on Medicare and lower prescription drug costs for beneficiaries. However, the implementation of the redesigned Medicare Part D program has led to various consequences for Part D plan sponsors (PDPs), beneficiaries, and manufacturers.

The IRA is making key changes to the Part D benefit design starting January 1, 2025:

-

- Elimination of the Coverage Gap: The coverage gap will be removed, leaving three phases: annual deductible, initial coverage, and catastrophic coverage.

-

- Changes in Drug Cost Sharing: Liability for drug costs will shift significantly between beneficiaries, PDPs, manufacturers, and CMS.

-

- Capping Out-Of-Pocket Costs: Beneficiaries’ annual out-of-pocket costs will be capped at $2,000.

-

- Revised TROOP Calculation: Costs counted towards True Out-Of-Pocket Costs (TrOOP) will include supplemental Part D coverage and other health insurance.

-

- Medicare Discount Program: A new discount program replaces the Coverage Gap Discount Program, with manufacturers offering discounts at different coverage phases.

-

- Reinsurance Changes: Different reinsurance calculations for Applicable and Non-Applicable Drugs will impact payments to PDPs.

For more details, see the CMS Fact Sheet.

These changes shift financial risks towards PDPs, potentially impacting premiums and formularies.

Impacts on PDPs

In 2024, PDPs submitted bids for 2025, factoring in the new benefit design. CMS addressed concerns in its Final Calendar Year Part D Redesign Instructions. The redesign especially impacts PDPs with many beneficiaries hitting the $2,000 out-of-pocket maximum.

Pressure on Premiums

Despite concerns about premium increases, CMS noted that the IRA’s premium stabilization limits annual increases to 6%. PDPs might still raise premiums to cover the increased financial risk.

Pressure on Formularies

The redesigned benefit reduces incentives for PDPs to favor higher-cost drugs. This could lead to changes in formulary designs, including placing certain drugs on non-preferred tiers or using utilization management tools.

Impacts on Beneficiaries

-

- Premiums: Financial pressure on PDPs may result in higher premiums.

-

- Formularies:

-

- Lower-cost drugs may be favored, potentially lowering point-of-sale cost shares.

-

- Increased use of utilization management tools could frustrate beneficiaries.

-

- Formularies:

-

- Capping Out-of-Pocket Costs: Beneficiaries with high drug costs will benefit from the $2,000 cap.

-

- Changes in True Out-of-Pocket Costs: Some beneficiaries may reach the out-of-pocket maximum faster.

Impacts on Manufacturers

Manufacturers will experience varied outcomes from the Part D redesign. Brand drug manufacturers may welcome the shift from the Coverage Gap Discount Program to the Medicare Discount Program. The out-of-pocket cap may increase demand for maintenance drugs. The overall changes in formularies might benefit manufacturers with lower-cost drugs, while others may face reduced rebates on Selected Drugs.

For a comprehensive understanding, view the Draft CY 2025 Part D Redesign Program Instructions.

—

Read More Kitchen Table News